America’s trusted debt relief company.

No obligation. Free consultation. $0 up-front fees.

Reduce what you owe.

Pay down $25,000 est. in debt faster than minimums (including interest)

Pay less each month

Liberty Debt Relief

$467

Current

$730

Reduce what you owe

Liberty Debt Relief

$22,400

est. total cost w/ fees

Current

$51,386

est. total cost w/ fees

Get rid of debt faster

Liberty Debt Relief

4 years

Current

5 years 9 mos

Clients could free up $263/mo (avg) compared to minimum debt payments.

Information provided in this graph is for informational purposes only and the Liberty Debt Relief option does not constitute an offer for debt resolution or any other product.

Our Process is Simple.

We’ve helped over 31,000 customers overcome debt—let us do it for you.

Review Your Situation

Talk to a Certified Debt Consultant at Liberty about your debt situation.

Discover Your Savings

Let's work together on a plan to reduce and manage your debt.

Enroll in the Program

Join our debt relief program and let us settle with your creditors.

We’ve helped resolve over $100 million in debt*

The goal is to create a plan that’s right for you.

Grow

Take charge of your finances with our FDIC-insured savings plan while we tailor a strategy to eliminate your debt.

Negotiate

Once you save enough, we’ll negotiate with creditors to settle your debts for less, paving the way for financial freedom.

Settle

Our expert negotiators work to settle your debts while securing your approval before finalizing any agreements with creditors.

Eliminate your debt and achieve financial liberty.

Continue*Total debt relieved between Liberty Debt Relief and it's partner debt relief companies.

Our experts are here to guide you.

We have over 50+ years of combined expertise in our field.

Frequently Asked Questions

Who is Liberty Debt Relief?

Liberty Debt Relief has been a trusted leader in debt relief nationwide for over seven years, offering proven solutions to help you regain control of your finances. We specialize in relieving unsecured debts like medical bills, credit cards, and personal loans—so you can move toward a debt-free future with confidence.

We respond to debt relief inquiries within hours, helping you quickly take the first step toward financial freedom. Speak to us 24/7 by calling 800-756-8447.

Can I trust Liberty Debt Relief?

Liberty Debt Relief prioritizes trust by actively listening to clients and tailoring debt relief solutions to their needs. Committed to exceptional customer care, Liberty Debt Relief has earned top ratings and accreditations, including an A+ from the Better Business Bureau (BBB) and thousands of five-star reviews across major platforms. Liberty Debt Relief stands as an industry leader with a proven track record of helping consumers resolve nearly a billion dollars in debt. We are also accredited by major organizations like the AADR, emphasizing ethical and effective service.

What debt relief services does Liberty Debt Relief offer?

Liberty Debt Relief and our affiliates offer tailored solutions—whether it’s debt relief, consolidation, or personal loans through a trusted partner—designed to align with your budget and financial goals.

Get a Free Personalized Evaluation of Your Debt Relief Options

Debt isn’t one-size-fits-all, and neither is our approach. Our free evaluation helps you compare options tailored to your unique situation, whether through our services or trusted partners.

Expert Support Every Step of the Way

Our team of Certified Debt Consultants and Client Support Specialists will guide you and assist you every step of the way.

Join thousands of individuals who trust Liberty Debt Relief to break free from debt and take back control of their finances.

Which is the best debt relief solution for me?

Liberty Debt Relief offers customized solutions to help you reduce debt to fit your budget and goals, including debt relief, but also solutions for personal loans and debt consolidation through our trusted partners. To ensure you find the best option, we provide a free debt evaluation that reviews all available solutions—whether through us or one of our trusted partners. Our team of Certified Debt Consultants, Debt Negotiators, and Customer Support Representatives will guide you at every step, with access to legal support if needed.

Unlike debt consolidation loans, our debt relief program is easier to qualify for, doesn’t require good credit, and helps you pay less on your total debt without added interest. However, if you’re still interested in a loan, our partner affiliates can check your eligibility for a debt consolidation or personal loan. No matter your situation, we’re here to help you find the best path toward financial freedom.

To discuss your unique situation, please speak with our Certified Debt Consultant by calling 800-756-8447.

How does Liberty's debt relief program work?

Liberty Debt Relief can help you reduce your debt in as little as 24-48 months.

- You make one low monthly deposit into a Dedicated Account that you control to fund future settlements.

- Once enough funds are saved, our team negotiates with creditors to lower your debt.

- After you approve a settlement, payments are made from your Dedicated Account to resolve the debt, along with our program fee.

*Note: The Dedicated Account is under your name and control. Once you authorize us to use it to pay each negotiated settlement, your paid-off accounts should reflect a balance of $0.

What type of debts can qualify for the program?

Our debt resolution program assists with unsecured debts—those not secured by collateral, such as a house or car. Some examples include:

- Credit cards & retail store cards

- Medical bills

- Most personal loans

- Collections and repossessions

- Lines of credit

- Some payday loans

- Certain private student loans

We are unable to assist with taxes, utility bills, lawsuits, secured loans, or federal student loans. To discuss your unique situation, please speak with our Certified Debt Consultant by calling 800-756-8447.

What does Liberty's Debt Relief program cost me?

Liberty Debt Relief ensures that our program is affordable for you by reviewing your budget and allowing you to customize your deposit schedule.

Our debt relief program helps you resolve debt for less than you owe, often faster than making minimum payments—without requiring good credit or upfront fees. A Certified Debt Consultant will guide you through your options, and once enrolled, you’ll have a plan with one low monthly payment.

You may terminate the program at any time without any termination fees.

Need an agent?

Our team will help you find the right solution.

Learn more about your financial options before making a decision.

At Liberty Debt Relief, our debt settlement service focuses on negotiating with your creditors to reduce the amount you owe. This process can be complex and stressful to face alone. Our experienced team guides you every step of the way, leveraging our knowledge of creditor negotiations to pursue a significant reduction in your debt. We will keep you informed and in control as we work on your behalf to achieve a fair settlement. Every financial situation is unique, and we tailor our approach to fit your needs. Regain control of your finances—contact us for supportive guidance and a free consultation.

Debt consolidation involves combining multiple debts into one, often through a new loan that pays off your unsecured balances. It can simplify your payments and potentially secure a lower interest rate or monthly payment. This strategy can ease stress, but it’s not a one-size-fits-all solution. At Liberty Debt Relief, we guide you through the pros and cons to determine if consolidation is right for you. Our advisors help create a personalized plan that fits your unique situation, exploring alternatives if needed. We’re here to answer your questions and support your journey—reach out for a free consultation to discuss your options.

Debt relief is about finding a sustainable way out of overwhelming debt, and our team is here to help you identify the best path. At Liberty Debt Relief, we draw on experience to analyze your situation—whether it involves credit card balances, personal loans, or medical bills—and develop a personalized strategy. We understand how hard it can be to recover from financial setbacks, so we focus on solutions that fit your life and goals. Our compassionate experts guide you step by step toward regaining stability and confidence. Take the first step toward financial freedom by contacting us for a free consultation.

High-interest credit card debt can quickly spiral, with balances growing despite your best efforts to pay them down. If your payments barely dent the principal, it may be time for a new strategy. Liberty Debt Relief helps you confront credit card debt by reviewing your situation and recommending relief options suited to you. From negotiating lower balances to consolidating your cards into one manageable plan, our team tailors the approach to your needs. We know how stressful it is to be stuck in debt, and we’re here to support you. Take the first step toward relief with a free consultation.

Eliminate your debt, achieve financial liberty.

ContinueKeep your debt

in check.

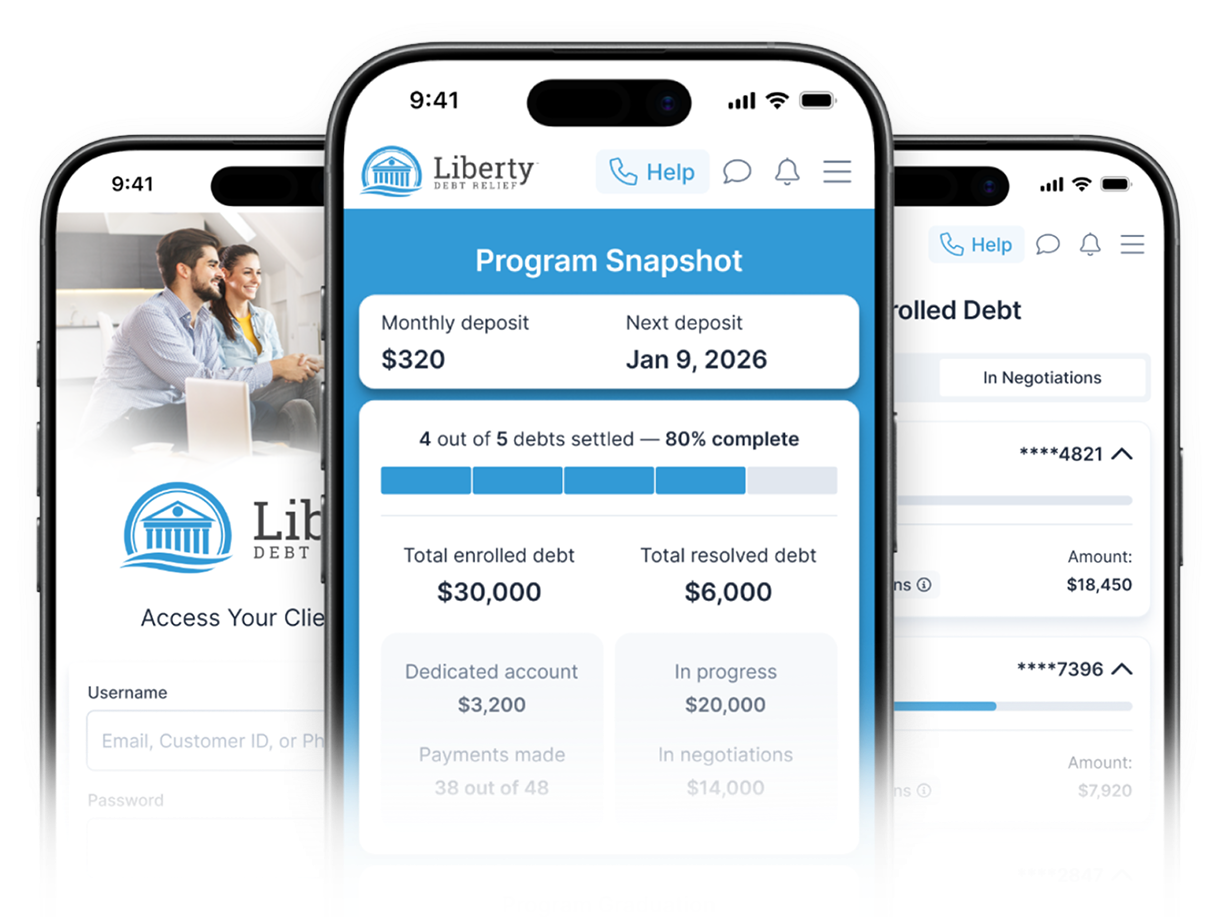

Introducing the Client Dashboard.

Make or skip payments, add new creditors, upload documents, update accounts, and much more—all in one place.

Red Dot

Red Dot

It’s time to prioritize your financial freedom.

We are committed to meeting your financial needs as your debt partner.

Simplified Process

We offer a catered debt relief program experience that fits your financial needs.

Experienced Staff

Our team comprises of professionals who have been working in the debt relief industry for over 15 years.

Expert Negotiators

Our skilled negotiators specialize in securing debt resolutions from top-tier financial institutions in the USA.

24/7 Support

We offer a catered debt relief program experience that fits your financial needs.

Industry Relationships

We have established connections with multiple creditors and lenders within the financial market.

100% Transparency

We have a trust and review system in place for you to verify us before making any financial decisions.

As a principal firm in the industry, we’re always looking for new talent.

Work from home, come to the office, set your hours—we’re flexible.

Manage Your Debt Relief – All in One App

Our new mobile app gives you a clear, secure way to stay connected to your debt relief program. Review enrolled accounts, track progress, upload documents, manage payments, and receive important updates

Screens shown are for demonstration only. Results may vary by individual.

How We Communicate

We may contact you via phone, email, or SMS regarding your inquiry, account updates, and service information. SMS consent is optional and not required to use our services.